Mat Credit Entitlement Calculation

Surcharge And Cess Is To Be Calculated After Deducting Mat Credit U S 115jaa From Tax On Assessed Income

Guide To Minimum Alternate Tax For Ind As Compliant Companies

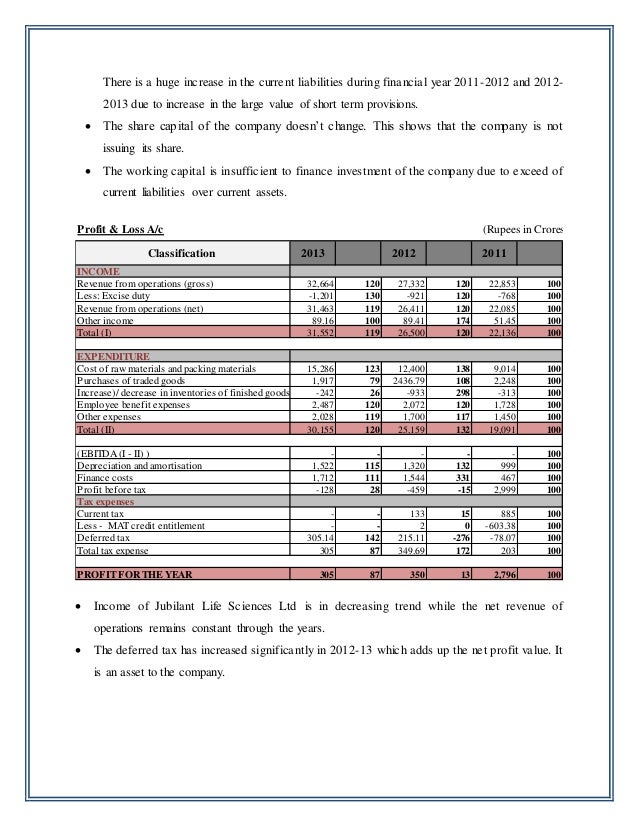

Common Size Trend Analysis Of Financial St Of Pharma Co

Https Assets Kpmg Content Dam Kpmg In Pdf 2020 01 Chapter 1 Aau Tax Ordinance Pdf

How To Calculate Your Cpp Retirement Pension Retire Happy

Https Www Bmcc Cuny Edu Library Wp Content Uploads 2019 10 Bmccbulletin9698r Pdf

What is mat credit.

Mat credit entitlement calculation.

Http Www Nishithdesai Com Fileadmin User Upload Pdfs Research 20papers Mergers Acquisitions In India Pdf

30 Best Stephen King Quotes Encouragement Quotes Stephen King Quotes Best Encouraging Quotes

Https Www Unison Org Uk Content Uploads 2019 06 Salary Sacrifice Pdf

Pin By Judith Machuca On Genevieve Name Names With Meaning Meant To Be Names

Https Www Pwc In Assets Pdfs Publications 2018 Ind As Presentation And Disclosure Checklist 2018 Pdf

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

2

Https Www Nhmrc Gov Au Sites Default Files Documents Attachments Enterprise Agreement 2019 Pdf

Https Www Cipla Com Sites Default Files Cipla 20ar 202018 19 2 Pdf

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Https Link Springer Com Content Pdf 10 1007 2f978 981 10 1452 9 Pdf

If A Company Is Showing Losses Does It Get A Tax Exemption In India Quora

Iaecqjdgrstwpm

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

What Is A 12 Month Period Under Fmla

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Waiver Of Cooling Period Under Sec 13b 2 Of Hindu Marriage Act 1955 Family And Matrimonial India

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Pin By Karma Love On Never Again Narcissistic Abuse Double Bind Narcissist

Source : pinterest.com