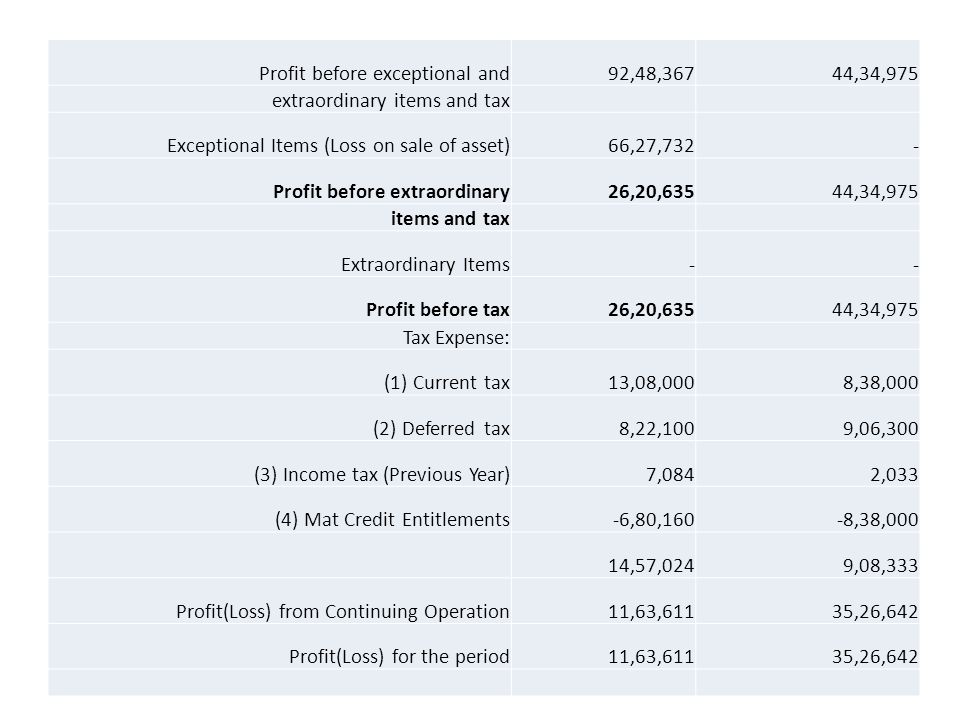

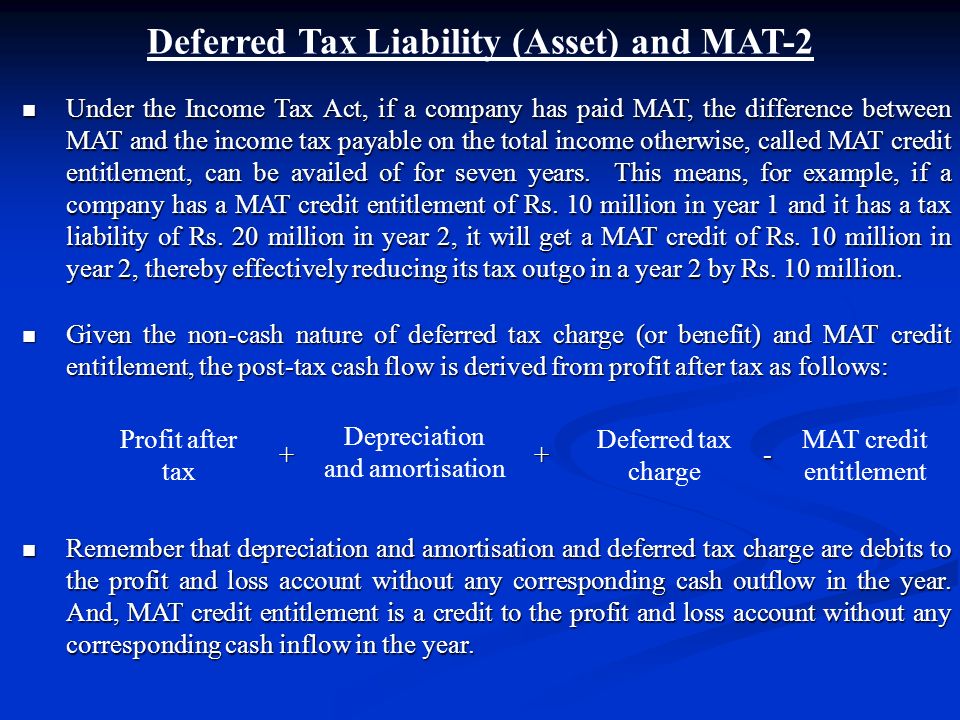

Mat Credit Entitlement Example

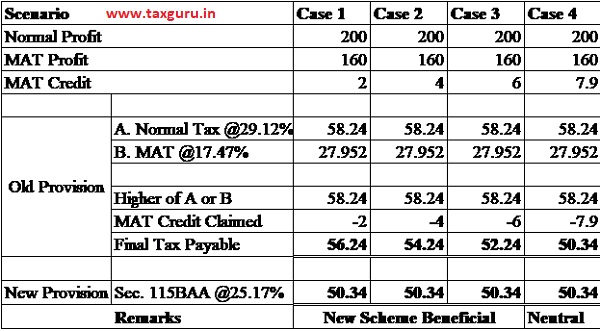

New Corporate Taxation Regime Section 115baa Mat

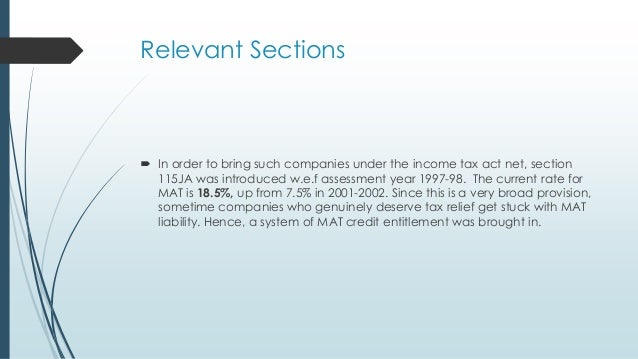

2 Intricacies Of Alternate Minimum Tax Sec 115jc Minimum Alternate Tax Sec 115jb By Pawan Singla Ppt Download

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Minimum Alternate Tax Mat Section 115jb

The Bane Of Mat Credit

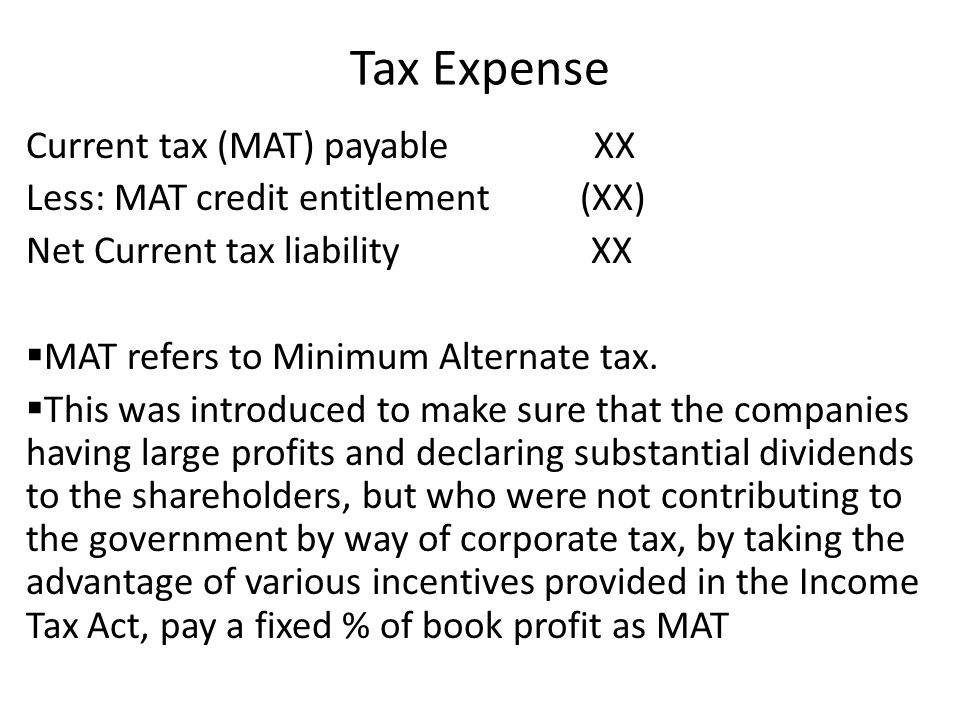

Minimum Alternate Tax

Provision for taxation a c dr.

Mat credit entitlement example.

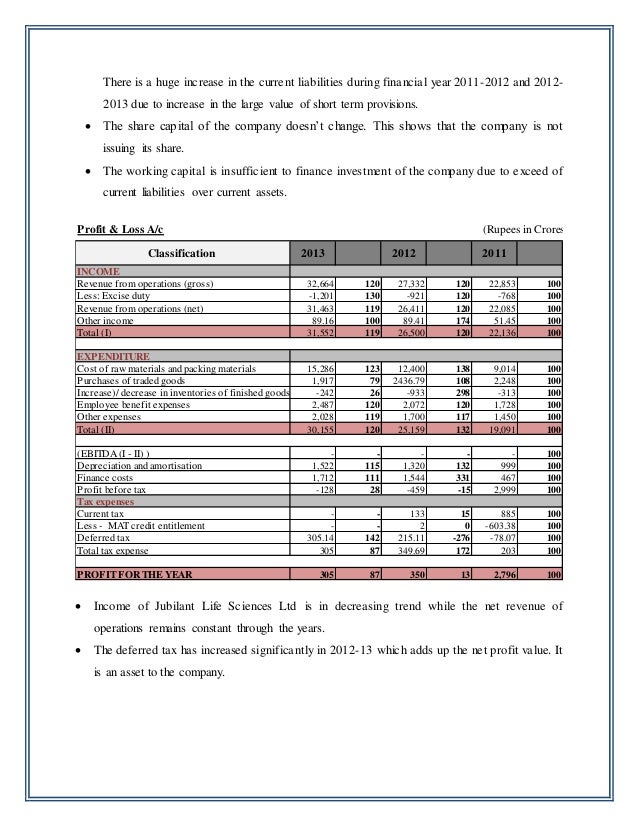

Common Size Trend Analysis Of Financial St Of Pharma Co

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Sutlej Textiles Industries Fundamental Analysis Dr Vijay Malik

Chapter 9 Project Cash Flows Ppt Video Online Download

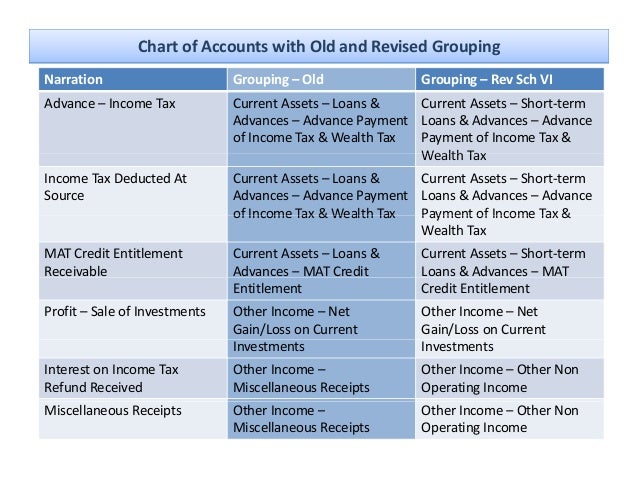

Revised Schedule Vi Print Disabled 1

Gopal Kavalireddi On Twitter In Fy20 Only 63 Companies Paid Tax Made Tax Provisions Greater Than 500 Crore Of The Bse Listed Entities Only 788 Companies Have Made Any Sort Of Tax Provisions

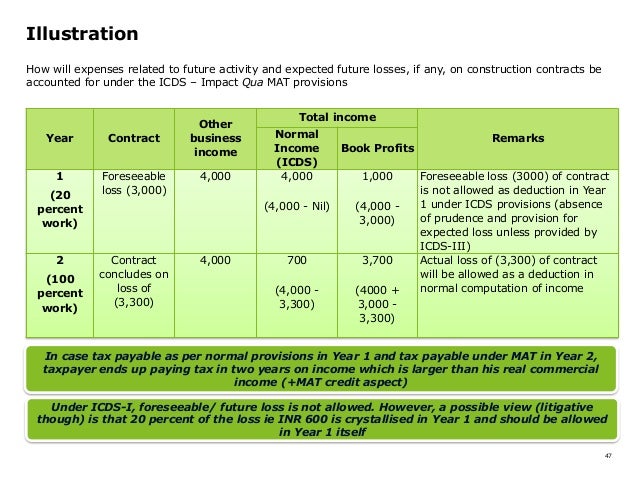

Session On Icds I To X Sandeep Jhunjhunwala

Balance Sheet As Per Companies Act Ppt Video Online Download

Significant Accounting Policies Mindtree

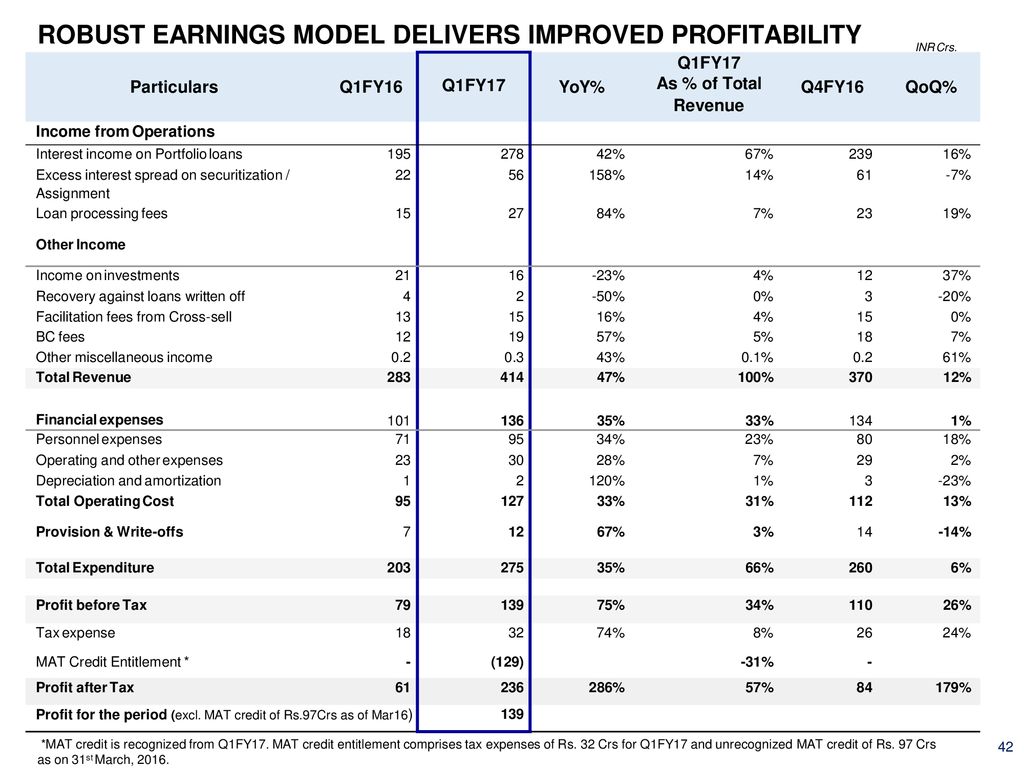

Earnings Update Q1fy17 July 2016 Sab Se Sastha Loan Ppt Download

Datamatics Global Services Ltd Fundamental Analysis Dr Vijay Malik

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Rule 11ua 1 C B Valuation Challenges And Our View Independent Valuation Services

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Firms Opting For Lower Tax Regime Can T Adjust Accumulated Credits On Mat Business Standard News

As 22 What Is Mat Credit Youtube

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

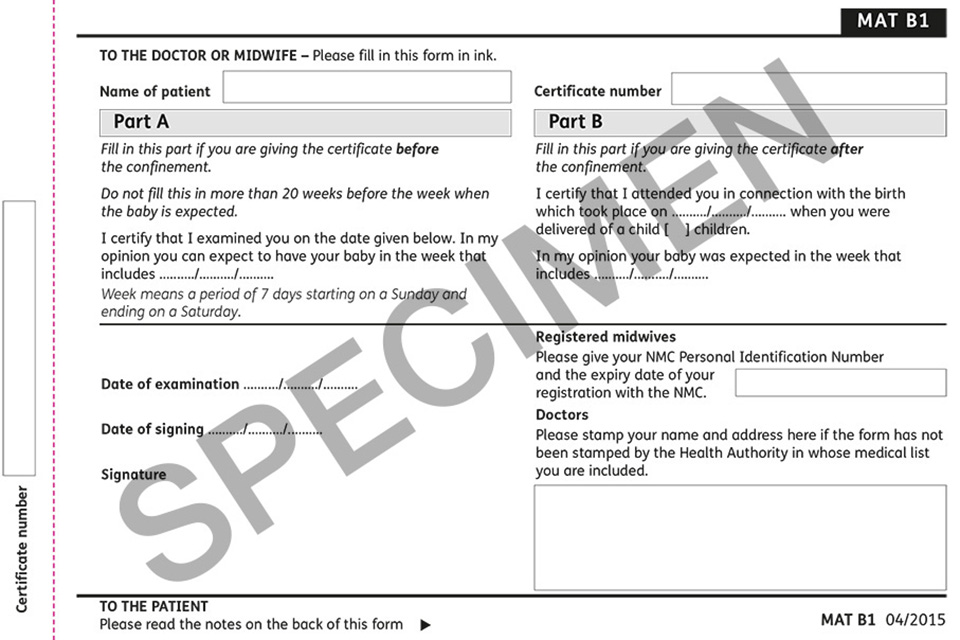

Maternity Certificate Form Mat B1 Guidance On Completion Gov Uk

Gayatari Projects Ltd Ar 2018 2019 Pages 101 150 Flip Pdf Download Fliphtml5

Https Www Borosil Com Site Assets Files 3299 Business Standard English Mumbai Edition Compressed Compressed Pdf

Http Www Bombaychamber Com Admin Uploaded Download Bcci 20prebudget 20memorandum 202020 Pdf

Https Www Pfizerindia Com Enewswebsite Investor Pdf Schemeofamalgamation Scheme 20of 20amalgamation Pdf

Mat Vs Amt Minimum Alternate Tax Alternate Minimum Tax Indiafilings

Https Assets Kpmg Content Dam Kpmg In Pdf 2020 01 Chapter 1 Aau Tax Ordinance Pdf

Source : pinterest.com